- Monthly Musings

- Posts

- Financialization of Indian Savings

Financialization of Indian Savings

Supratik Sarkar

December 01, 2022

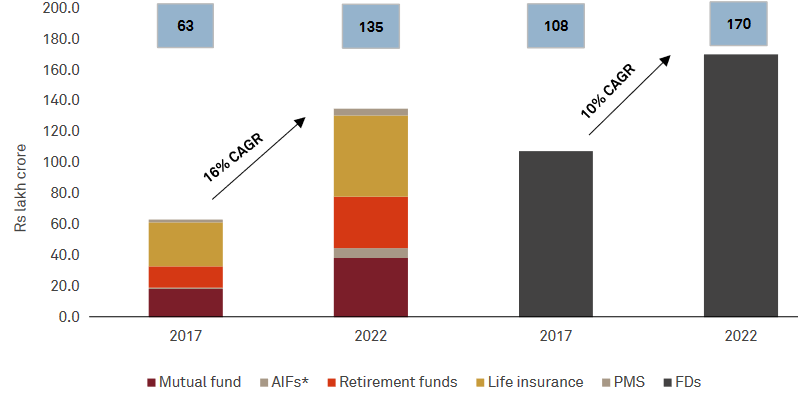

India's efforts towards financial inclusion, digitization, & rising middle-class disposable incomes have led to an increase in household savings being channeled towards the managed investments industry. Life insurance comprises the largest share (39% @ Rs. 52 Lakh Cr+), followed by mutual funds (28.4% @ Rs.38 Lakh Cr+). Due to the increasing inflation, households are now looking for investment options that offer higher returns than fixed deposits. Despite the fact that fixed deposits only make up approximately 10% of households' gross financial savings, there has been a significant shift away from bank deposits.

Managed Investment solutions gain footing on FDs, the usual trusted choice of Indians beyond gold & real estate. Source: AMFI, IRDAI, SEBI, CRISIL, NPS Trust, RBI, IMF

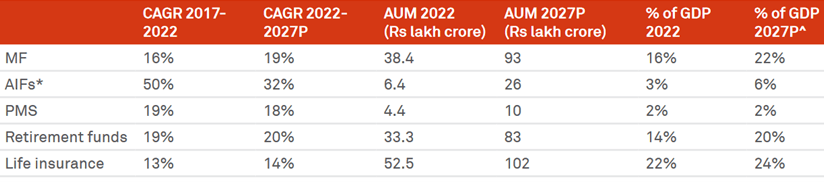

Rapid growth in every vertical of this industry. Source: AMFI, IRDAI, SEBI, CRISIL, NPS Trust, RBI, IMF

The managed investments industry's total assets are Rs. 135 lakh Cr. (~57% of GDP) as of March 2022, expected to 2x to Rs. 315 lakh Cr. (~74% of GDP) by March 2027. This puts the AUM in this industry already at ~79% of the AUM under FDs v/s 59% just 5 years ago showing the rapid rate of change in India’s preferred asset allocation. Evident shows domestic investors are increasingly looking at managed investment solutions as an alternative to park their money.

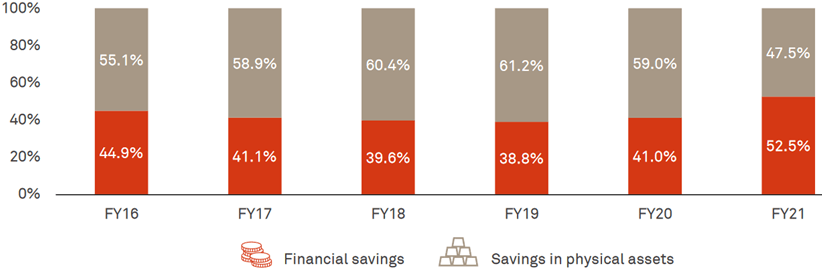

Share of financial savings increase. Source: RBI, CRISIL

Macro drivers for this systemic trend

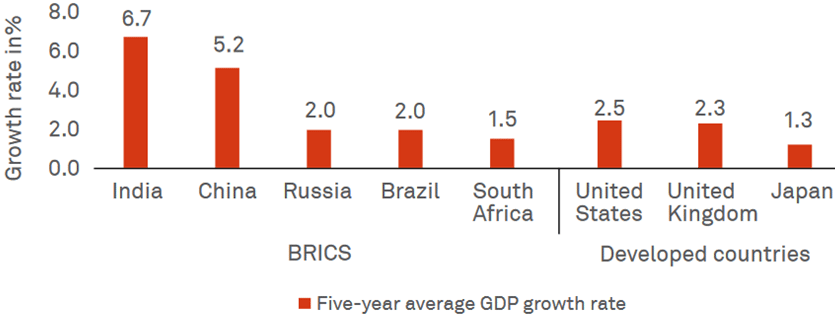

India was among the fastest-growing major economies in the world before the pandemic (~6.7%, 2014-2019). The IMF predicts that India's GDP will grow faster than other economies possibly even faster than China. Indian corporates especially large ones with moat have a strong balance sheet that can help kick-start private investment, & the Production-Linked Incentive scheme incentivizes manufacturing investments. Govt.'s focus on infrastructure investments has a multiplier effect on the economy, & the well-capitalized banking sector with low non-performing assets supports economic growth. Faster digitalization provides citizens with greater access to opportunities & a platform for innovation while cutting leakages through targeted delivery of services. The current trend of financialization of savings will only increase the access to low-cost capital for corporate India to boom.

India is the fastest growing economy. Source: IMF July 2022 World Economic Update

India's per-capita income crossed $2,000 in 2021, the inflection point where income moves towards spending & investments. Additionally, the proportion of middle-income households in India is projected to reach 18.1 crore by fiscal 2030, 1.5x the number of households in the US. India also has a large young population, with about 94 crore people in the working age group, & is expected to contribute 22.5% of the incremental global workforce over the next decade. India's financial inclusion has improved significantly from 2014-2023, with the share of adults with a bank account rising from 53% to >90% due to government measures such as the Aadhaar & Jan-Dhan program. This has led to an uptick in the generally high domestic savings rate to go even higher to 29.3%, v/s global average of 26.9%.

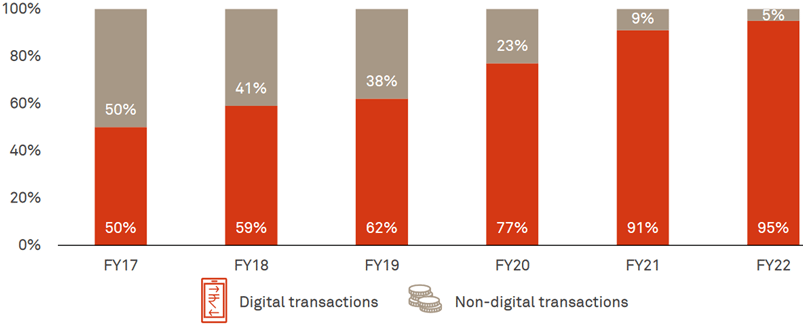

Technology has helped surmount challenges due to India's vast geography, making it commercially nonviable to have physical footprints in smaller locations. The shift towards digital channels & e-commerce was accelerated by demonetisation, GST & the Covid-19 pandemic. The usage of technology has also resulted in a rising number of DIY investor who invest through direct mutual funds or zero cost brokers to directly invest in stocks further improving market liquidity through retail participation.

Financial Transactions by Volume. Digital transactions: RTGS (excluding interbank clearing), ECS, NEFT, IMPS, NACH, cards & prepaid instruments; Non-digital: Cheque/paper clearing, ATM. Source: RBI, CRISIL MI&A Research

Passive funds are becoming popular in India due to the better returns factoring for lower fees & expenses. Their share in AUM has grown from 3% to ~13% in March 2022, driven by institutional investors like PFs. This trend is expected to continue with individual investors also showing interest in passive funds due to the declining alpha of actively managed funds. The rise in the share of passive funds in the Indian MF industry is similar to global trends, with the US at 43% & Asia ex-Japan at 32% in 2021.

At the macro level, the pace of technology & intermediation will continue to be crucial in driving product penetration. The rise of a sticky domestic capital market, also protects the overall market from the hot flows of foreign investors. The financialisation of household savings, prospects of strong economic growth, access to capital market products, emergence of technology, growth of middle-income households, young demography, improved financial literacy, access to information, & awareness provide a boost to the investment climate. That said, financialisation of assets & its increasing flow into the managed investments industry has been backed by buoyant debt & equity markets fueled by excessive liquidity.

Some of my other favorite articles about the Indian economy -

This will be my last newsletter for this year, I want to deeply thank all my readers for your continued support, insightful feedback and I hope to continue to add more value to you in the coming years. Thank you 💕🙌

Source: CRSIL December 2022 report - “The big shift in financialisation”

Disclaimer: The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide education about the financial industry. The views reflected in the commentary are subject to change at any time without notice. Nothing on this Blog constitutes investment advice, performance data or any recommendation that any security, portfolio of securities, investment product, transaction or investment strategy is suitable for any specific person. From reading this Blog we cannot assess anything about your personal circumstances, your finances, or your goals and objectives, all of which are unique to you, so any opinions or information contained on this Blog are just that – an opinion or information. You should not use this Blog to make financial decisions and we highly recommended you seek professional advice from someone who is authorised to provide investment advice.