- Monthly Musings

- Posts

- India's journey to $10Trillion economy

India's journey to $10Trillion economy

Supratik Sarkar

November 01, 2022

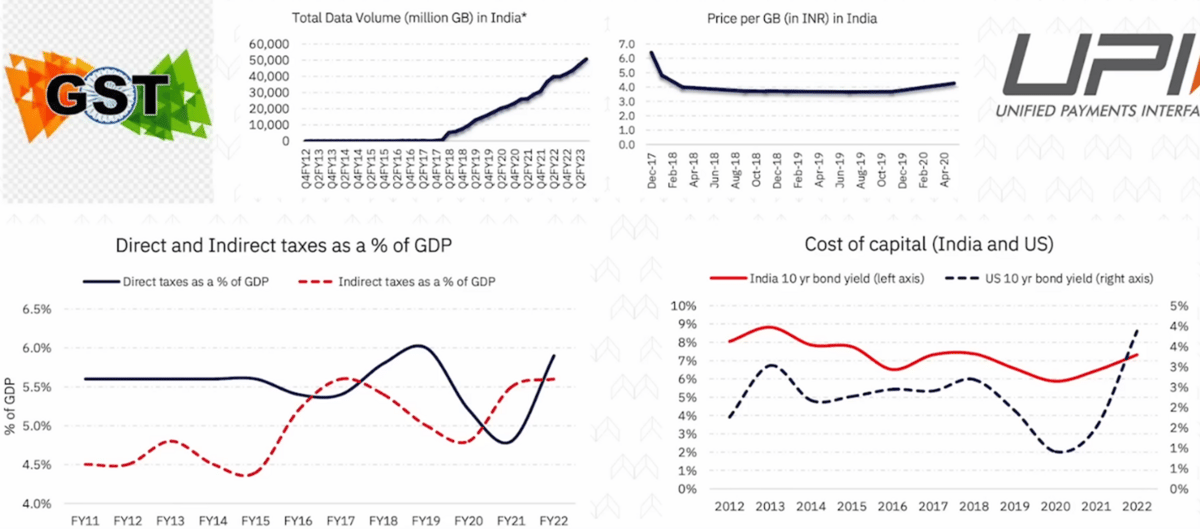

Infrastructure development will be the gunpowder for India to become a $10trillion economy. Despite having only 45% smartphone penetration, India generates more mobile data than Europe & USA combined. Broadband usage & bank accounts increase has been accompanied by a decrease in journey times due to the construction of a highway network aided by FasTag (reduced average wait time from, 8 mins to <40 seconds). Tax reforms have revolutionized the economy, specifically the reduction in the corporate tax rate from 35% to 25% in September 2019. Despite this reduction, tax collections, particularly direct tax collections as a percentage of GDP, have hit all-time highs, GST & demonetization has rapidly increased the rate of formalization of every sector.

New sources of India’s competitive advantage, Source: Marcellus Investment Managers, Bloomberg

Almost 99.9% of India’s entire adult population have an Aadhar. UPI has greatly impacted the banking & finance industries making financial transactions exponentially easier & accessible for people, especially for small & medium-sized enterprises (SMEs). The collection of data through retail apps (the moment a brand/company app say Dominos Pizza App, is installed on an Indian phone, data is scraped from SMSes, chats, locations the phone has been in etc, logged & then sent to that company) provides banks & companies with valuable information that they can use to make more informed lending decisions using machine learning algorithms. This result in lower lending rates for low-risk customers, but higher rates for those who don't display low-risk behaviours on the banking side & better targeted customer marketing on the retail sales side.

The rise of these Digital Public Goods (DPGs) will significantly ease lending for banks & non-banking financial companies (NBFCs) due to the JAM (Jan Dhan, Aadhaar, Mobile) trinity. Increased data usage & insights from consumption patterns of such a large populace using UPI when leveraged with the Account Aggregator (AA) framework & end-to-end digital access to key documents (e-Aadhar, e-sign, digilocker), will revolutionize credit underwriting & loan disbursement-collection. Lower turnaround times, increasing efficiencies & better quality of loans will mean lesser gross NPAs on a systemic scale for the country thus boosting credit cycles on a massive scale.

Open Network for Digital Commerce (ONDC), allows customers to purchase goods from any vendor in the country, regardless of whether they are on a platform. It provides customers with more options & greater control over the payment & delivery process & provides sellers with greater visibility without having to be dependent on the existing large players that enjoy visibility. A robust logistical supply chain network, enabled by FASTag & GSTN, should pave the way for a faster & more cost-effective logistics ecosystem in India. As credit cycles improve, more efficient logistics/supply chain fulfillment, & eCommerce democratization kicks in, it will become less attractive for firms to operate in the black economy. The faster formalization of the SME sector will lead to increased savings being invested in financial assets rather than physical ones.

A 2017 RBI survey revealed ~95% of Indian household savings are in real estate & gold, ~5% in financial assets. Physical assets which has usually worked well before, now isn’t expected to generate returns above the cost of capital when factoring in inflation thus signalling a massive wave of financialization of Indian savings to the tune of $1 trillion even assuming just a 1% per annum shift from physical to financial assets, reducing the cost of capital further. This means India’s cost of capital is unlikely to shoot up as rapidly as other developed economies’ have (like US, UK) in their efforts to curb inflation. Indian companies thus stand the chance to get even more competitive on the global stage.

Networking of India and polarizing of Indian economy means massive opportunity for consolidators, Source: Marcellus Investment Managers, Bloomberg, Ace Equity, IIFL Capital

India has a competitive advantage in knowledge-intensive, capital-light industries & that companies in these industries can become world leaders if the economy continues to develop. This combined with existence of dominant players in Indian markets that have consistently had ROCE>15% & sales growth>10% every year for the last decade or so with a wide enough moat, provides an opportunity for investors to ride the inevitable stock market boom since share prices compound similarly to EPS growth. Overall, there is transformative power of technology in India & its potential to drive economic growth & improve the lives of people has just started to be seen.

Sources:

https://www.youtube.com/live/oOJB14ZSEp4?feature=shareDisclaimer: The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide education about the financial industry. The views reflected in the commentary are subject to change at any time without notice. Nothing on this Blog constitutes investment advice, performance data or any recommendation that any security, portfolio of securities, investment product, transaction or investment strategy is suitable for any specific person. From reading this Blog we cannot assess anything about your personal circumstances, your finances, or your goals and objectives, all of which are unique to you, so any opinions or information contained on this Blog are just that – an opinion or information. You should not use this Blog to make financial decisions and we highly recommended you seek professional advice from someone who is authorised to provide investment advice.