- Monthly Musings

- Posts

- Risk & opportunities of expensive money

Risk & opportunities of expensive money

Supratik Sarkar

April 01, 2023

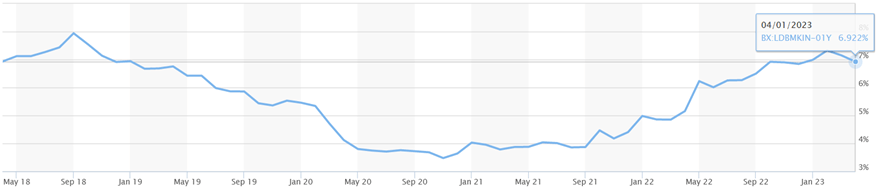

Indian 1Y T-bill yield was 6.92% as of April 1, 2023. Source: Marketwatch.com, RBI

This means that Govt. has to pay 6.92% interest to borrow money for 1 year, almost the 2nd highest rate since 2015. Indian Govt. 1Y bonds are considered to be the safest asset class for the domestic investor & consequently for any borrower other than Govt., they have to cough up a yield better than what the safest asset can offer. Thus, cost of funding for all corporates have exponentially shot up in the last few years. Additionally, Indian Govt.’s already massive fiscal deficit balloons up even more with a larger interest payment on bonds, which trickles down for the citizens as a massive financial burden in the form of higher inflation (which corporates will pile on too to maintain their profit margins since their cost of funding have gone up) & higher taxes. Both the quantum of savings post taxes & the purchasing power of said savings have gone down. But this also provides a somewhat rare opportunity because inflation is at 6.44% which means when invested correctly, money can grow at a much faster rate than the reduction of purchasing power.

The 2020 Covid pandemic led to widespread lockdowns & supply chain disruptions, which caused a severe liquidity crisis worldwide. In response, central banks, including RBI, lowered interest rates & provided liquidity to the markets by pumping money into the financial system. RBI introduced “Targeted Long Term Repo Operations (TLTRO)” program to provide support to banks wherein 73,000 Crores (~$10 billion USD) were provided to banks at rates as low as 4.4%, for 3 years, to invest in specific sectors of the economy, thereby supporting economic activity during a challenging time. These funds are now set to mature by the end of April, which means that banks will have to repay the borrowed amount. If banks are unable to repay the borrowed amount, it could lead to a liquidity crunch & impact the overall financial system. However, if banks are able to repay the funds, it could lead to a reduction in liquidity in the markets.

73,000 Crore worth bank loans from RBI set to expire by April 2023. Source: RBI

Currently, banks are parking this liquidity back with RBI at 6.25% in a “Standing Deposit Facility” discount window, which gives them 1.85% i.e.,1,300 crore rupees of “free” money. However, with the end of TLTRO, banks will lose this free interest, & have to borrow from the market, where rates are climbing rapidly. Short-term money, such as commercial paper & money markets, is already becoming more expensive for banks & corporates, rates climbing close to 8%. Even HDFC Bank which is considered to be the safest private bank in India, is paying 7.8% for a 300-day borrowing. Banks are raising deposit rates, which will soon lead to an increase in lending rates. The pace of deposit rate hikes is accelerating, & lending rates are increasing even faster.

Median lending & deposit rates for Indian banks, Source: RBI, CapitalMind

So where’s the opportunity here ?

Fixed income can be one path. Rates are expected to continue in the current range even if not shoot up exponentially, especially if inflation remains in its current elevated range. In the short term, bonds above 6 months duration yield at least 7% which means a good ultra-short/ low duration fund can generate inflation beating returns. You can even invest in shorter duration Govt. T-bills directly from RBI Retail direct platform. With the recent amendment removing indexation benefits for debt funds, longer term investments in interest risk assets need to be re-assessed to check if they can provide inflation beating returns when adjusting for expenses, taxes and risk.

Usually, stock markets suffer a lot due to interest rate hikes due to corporate leverage but this time, industrial leverage isn’t that high considering 5Y annualized credit growth for industrial loans is 12.88% v/s 16.71% for retail loans, loans to NBFCs at 27.92% & 14.81% for housing loans.

However, the rising interest rates & rapid growth in retail loans from both banks & NBFCs means chances of NPAs in is much higher now. Loans to start-ups, SMEs & new business stand a higher probability of default now, which also means that newer loans will be disbursed with less ease due to higher cost and risk. Liquidity especially for leveraged & new/small firms has now dried up & this trend will continue. This means the established corporate monoliths with a proven track record for profitability with low leverage will continue to dominate their industries, get bigger & usurp more market penetration from smaller, newer & unorganized players. Fundamentally robust companies & their stocks stand to soar higher than ever.

Thirdly, insurance premiums might go up for new insurers the higher the interest rates go up so if u expect interest rates to continue to rise this might be a good time to lock in rates for new plans. Finally, if you can do it, investment in yourself by upskilling is the best investment you will ever make no matter what macros are changing in global economy.

Disclaimer: The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide education about the financial industry. The views reflected in the commentary are subject to change at any time without notice. Nothing on this Blog constitutes investment advice, performance data or any recommendation that any security, portfolio of securities, investment product, transaction or investment strategy is suitable for any specific person. From reading this Blog we cannot assess anything about your personal circumstances, your finances, or your goals and objectives, all of which are unique to you, so any opinions or information contained on this Blog are just that – an opinion or information. You should not use this Blog to make financial decisions and we highly recommended you seek professional advice from someone who is authorised to provide investment advice.